How many times have friends or family members asked you, “have you been saving your money?”

It’s an incessant question, but one that many of us should be seriously considering – especially younger generations just getting started in their careers.

Saving money, more specifically saving money for retirement, has many upsides. Setting aside income early in your career could mean:

One of the top ways to save for retirement today is by contributing to a 401(k) plan. In this brief guide, we’ll discuss the benefits of a 401(k), why you should consider one if it’s offered by your employer, and how exactly they work.

A 401(k) is a retirement savings plan sponsored by an employer. It allows employees to divert a portion of their paychecks into a long-term investment account. A 401(k) is considered a “qualified” retirement plan, meaning it is eligible for special tax benefits under IRS guidelines.

The 401(k) plan was incepted in 1978, when Congress determined pensions were too expensive to maintain. The shift to 401(k) plans ensured companies didn’t have to provide a steady stream of income to their retired employees. Another idea behind 401(k) plans is that they allow employees to manage their funds with more flexibility.

However, there are different types of 401(k) plans, and understanding which one your employer offers is important.

So, you just started a new gig and lucky for you, the company offers a 401(k) retirement savings plan, now what?

Assuming you agree to sign up for the plan, you’ll be contributing a portion of your regular paycheck to your 401(k). The amount of money is determined by employees themselves, but the average for 2019 is about 3 percent.

Using the national average as an example, if your annual salary is $60,000 and you divert 3 percent to your 401(k), your yearly contribution equals $1,800.

It is, however, strongly recommended by financial professionals to contribute as much as you feasibly can to your 401(k) plan. Percentage-wise, this could be anywhere from 10-15 percent. Many companies that have 401(k) plans allow employees to manage their contributions using benefits administration software.

| Tip: While you should stay ahead of the curve for retirement savings, you’ll want to ensure you have enough money in your bank account for living expenses, leisure, and unexpected emergencies. For more insight about projecting your retirement savings, check out our free 401(k) calculator. |

Some 401(k) plans offer employer matching after you’ve spent a certain amount of time with the company – typically a few years to incentivize employees to stay longer.

Employer matching means your company will match your yearly contributions up to a certain limit (the most common being 3 percent). These limits will be laid out in the terms and conditions of your 401(k) plan.

Using our annual salary example of $60,000 and national contribution average of 3 percent, this would mean your employer would match that 3 percent – taking your contribution from $1,800 to $3,600.

Aside from setting yourself up nicely for retirement, employer matching is another key reason to take advantage of a 401(k). Otherwise, you’d essentially be leaving “free money” on the table.

Once you understand how a 401(k) works, the next step is finding the right platform to manage it. Here's what long-term users say about the most reliable 401(k) platforms on G2.

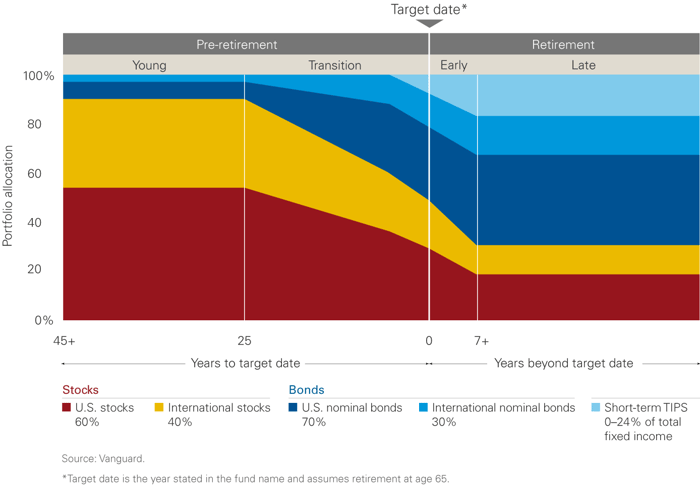

The benefit of a 401(k) versus stashing money in a mattress is its ability to generate enough money for retirement with minimal risk. This is most commonly done through target-date funds, or TDFs.

Target-date funds: TDFs are comprised of low-volatile stocks and bonds. They are designed to be the most reliable investment option since they become more conservative as employees get closer to their retirement age. TDFs are managed by financial services companies like The Vanguard Group or Fidelity Investments.

Below is an example of a TDF which began in 2015. You can see how the fund adjusts for risk at around the 25-year-before-retirement mark.

While TDFs are generally considered the most reliable investment option, employees aren’t handcuffed by them. Using your employer’s 401(k) administrator portal, you can see exactly where your money is distributed and make adjustments accordingly. Although, you should consult with your Human Resources department first.

Depending on the employer, there are a variety of 401(k) plans you could be presented with – the most common being a traditional 401(k) and the second being a Roth 401(k). Our graphic below shows some of the key differences between the two, with most of the differences based on how the money is being taxed.

| Traditional 401(k) | Roth 401(k) | |

| Tax rules | Contributions to the 401(k) from each paycheck are not taxed until withdrawal. | Contributions to the 401(k) from each paycheck will be taxed. |

| Withdrawal rules | No access to funds before age 59 ½ or if you leave your employer at age 55 or older. A 10% penalty + regular taxes will be applied for dipping in early. | Access to money with no penalty as long as the account has been held for 5 years. This allows for more flexibility. |

Other less-common 401(k) plans include:

| Related Content: Saving for retirement can be tough as a freelancer, and so is acquiring health insurance. Read our guide on self-employed health insurance to learn more about your coverage options. |

Retirement funds are retirement funds for a reason, so you probably shouldn’t be looking to withdraw from it until the time is right.

That being said, you typically can’t tap into your 401(k) until you’ve reached the age of 59 ½. Doing so beforehand will lead to a 10 percent tax penalty on top of the usual tax bill that comes with traditional 401(k) plans. This is a hefty amount of lost money.

You may be out of a job if your company goes under, but thankfully, your 401(k) will be safe and sound. In the unfortunate event that this happens, employees have the option to move their plan over to an Individual Retirement Account, also known as an IRA, without paying any income taxes on it. This ensures the safety of your retirement funds.

That sums up all the basics of a 401(k) and why you should consider enrolling in one if it’s offered by your employer.

Still looking for that dream job? The one with a competitive salary, great perks, and generous 401(k) matching? Here are 4 key transferable skills you can apply in multiple areas of your life to become the prime jobseeker.

Saving for retirement can be a daunting task, but your 50-year-old self will be thankful you...

by Devin Pickell

Human Interest, Guideline, and Betterment at Work are the best 401(k) software,based on G2's...

/DarshayitaThakur-OrangeBG.webp) by Darshayita Thakur

by Darshayita Thakur

Planning for the future is daunting, especially when the end goal feels out of sight.

by Maddie Rehayem

by Maddie Rehayem