Payment security is mission-critical for any company, especially now, when criminals and fraudsters look for security vulnerabilities to steal data.

Experts expect real-time payments to amount to over half a trillion transactions and show no signs of slowing down. That’s a lot of opportunity for cybercriminals.

Customers want the freedom to choose a payment method they trust, and online organizations must offer a flexible, secure, and easy-to-use experience. But, most online consumers will abandon their carts if they sense an e-commerce store is not secure, which can lead to a loss of revenue and negatively affect the brand’s reputation.

Here is what you need to know about online payment security to give your customers the best experience possible.

The payment processing landscape has changed dramatically in recent years. Companies would store credit card information on their own servers in the past. However, this made them a prime target for hackers.

Today, most businesses use a payment gateway as a middleman between them and the customer’s bank, which is often connected using APIs. Integrating an API management gateway here adds an extra layer of security for customers. Their credit card information is never stored on the merchant’s servers and is only processed via secure APIs.

Online businesses may opt for a payment processor, making it easy for customers to pay for goods and services online. This service will enable companies to power their services worldwide. Payment processors also provide a safe and secure checkout experience that boosts consumer trust.

What’s the difference? A payment gateway is a system that collects credit card information and ensures it’s valid.

Payment gateways protect sensitive information through encryption and tokenization by facilitating the secure transmission of payment data. So, a reliable payment gateway is crucial for ensuring the security and compliance of transactions.

Depending on the website, the payment gateway is either part of the site’s infrastructure (as an integration) or sends users to its own website (third-party payment gateway) and back to the merchant. After the payment gateway receives the credit card information, it sends it to the payment processor for verification.

So, think of the payment gateway as the first step in taking a customer’s payment information. The “gateway” connects the merchant, customer, and payment processor.

A payment processor handles the actual transaction. Once the payment gateway sends the payment information, the processor communicates with the customer’s and merchant’s banks to authorize, clear, and settle the payment.

While payment gateways focus on security, payment processors focus on authorizing and settling payments.

Payment methods were much simpler; you could pay with cash or a card. With the advancement of digital payment options, consumers can pay for their goods in several ways, from kid’s debit cards to digital wallets.

The most common types of payment methods are:

Merchants need a system that protects their customers regardless of their method. This applies not only to retail transactions but also to sectors like the mortgage industry for a home loan, healthcare, and insurance claims processing, where secure payment processing is vital to protect sensitive financial and personal data.

Customers:

Businesses:

Financial data is at high risk, especially in an increasingly digital world. Cyber criminals are attracted to financial data because of its value and vulnerability.

So, safeguarding information during transactions is mission-critical. This information includes credit card numbers, bank account details, and personal identification information (e.g., name, date of birth, social security number).

In 2024, the global average cost of a data breach was $4.88 million. In 2022, customers lost $8.8 billion to scams.

Many of the world’s leading financial institutions, including NASDAQ, Citibank, and PNC Bank, were hacked between 2005 and 2012. This hack was possible due to vulnerabilities with SQL injection exploits. SQL injection attacks can be avoided if companies use parameterized database queries.

One of the most significant advancements in payment security came in 2012 with PCI-certified peer-to-peer encryption, ensuring that confidential data is immediately secured. Before hitting the payment processing system, it must travel to a payment gateway through the merchant’s local network.

In 2016, hackers stole the personal information of 57 million Uber customers. The cyber criminals held Uber ransom for $100,000, which the company paid to delete the data. Thanks to significant advancements in payment processing security, hackers couldn’t gather any payment information during this attack.

Shopping has trended towards more online transactions with no signs of slowing down. The pandemic made businesses such as Reliable Couriers more reliant on online shopping. That’s why payment security is more critical than ever.

Now that you know more about payment processing security, how does yours stack up? Let’s examine how you can ensure your company follows the best practices. Doing so will help you build long-term trust and loyalty with consumers as they feel confident their sensitive information is safe with your business.

There are three things your business needs to work on to reduce risk at checkout:

Here are 10 best practices to ensure that your business reduces the risk of fraud.

The first step is to look at your current payment processing security measures. This includes understanding your type of payment gateway and whether it’s PCI-compliant.

Hackers are constantly evolving their craft, and new attacks are developed continuously. When it comes to payment security, you should use the best methods for keeping data secure.

Here are some factors you should assess your operation for:

Check that your current payment processing software is not outdated. If it does not meet the latest security standards, investing in an update or replacement is essential. Any company that sells products or services online will need payment processing software.

Internal data processing software should be secure. Customers must feel confident their information is safe when stored on your servers. Look for software that offers features like encryption and password protection.

Anti-fraud software can help stop criminals from accessing sensitive customer information. This type of software uses data analytics to flag suspicious activity and block fraudulent transactions before they happen.

Identity authentication is another essential layer of payment security. This helps to ensure that only authorized users can access payment information. Two-factor authentication is a great way to add an extra level of protection.

Address verification service (AVS) is also a valuable security measure for payment. This system checks the billing address against the one on file with the credit card company. If there’s a mismatch, it will flag the transaction as potentially fraudulent.

Looking for secure solutions that put these best practices into action? Check out the top-rated payment processing software for 2025.

Make sure your business is compliant by gaining the PCI compliance certification. You should meet the requirements set out by the Payment Card Industry Data Security Standard (PCI DSS).

Some of the best practices you’ll need to follow include:

PCI compliance is not a legal rule for a merchant to do business. It is a security request from major credit card companies, including Mastercard.

You should consider whether your operation complies with Europe and the UK’s GDPR. If you sell goods in Europe, this legal requirement can lead to hefty fines if not followed.

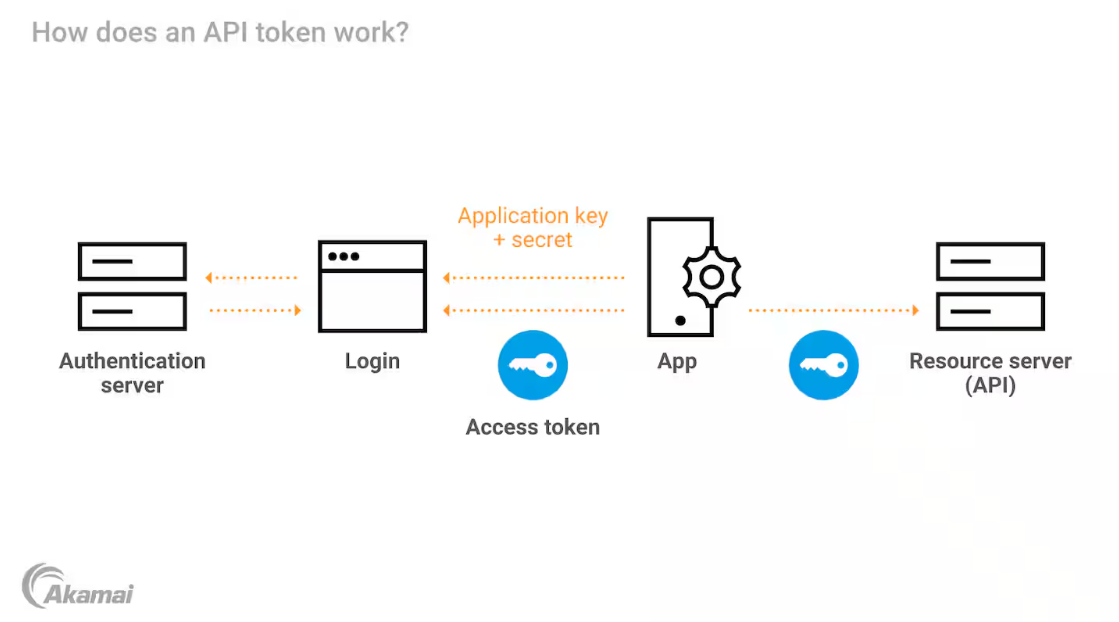

Another payment security method that’s becoming more popular is tokenization. This will replace sensitive data with a unique code for future transactions.

Source: Akamai

If a hacker were to gain access to this token, they could not use it to make purchases. The token itself has no actual value. Tokenization can be used for both in-person and online transactions.

For example, suppose someone purchases using a credit card with the number 3456 6484 4665 4942. This will be substituted with a dummy code such as hgh-2345ddih, which will be useless to hackers.

Encryption is a payment security measure that’s been around for quite some time. It works by encoding data so that only authorized users can decipher it.

Encryption protects both online and offline transactions in the payment processing world. Secure Sockets Layer (SSL) encryption is used for online payments. SSL encrypts data as it’s transmitted from the client to the merchant.

Savvy internet users will look out for SSL certification on websites they visit. They can identify this by a small padlock next to the URL of the website the user is on. Consumers can check the certificate’s details, including the issuer and expiry date.

Make sure that the SSL you are using is not outdated. The version you have should use Transport Layer Security (TLS). Once set up, you must run a new penetration test for vulnerabilities.

A payment processing security plan is only as strong as its weakest link. Hackers can exploit these issues to gain access to sensitive data or take control of systems. This is why scanning for vulnerabilities regularly and patching them as soon as they’re discovered is crucial.

Regular vulnerability scanning is an integral part of maintaining payment processing security. If you can find and fix issues quickly, there is less risk of attack against payment systems, and hackers will find it harder to compromise a business's defenses.

Businesses that allow payments through their apps benefit from following container security best practices. Containers package your app and everything it needs to run. If these containers aren’t properly secured, they can become a weak point that hackers might exploit, putting your payment system at risk.

By regularly checking these containers for security issues, you can spot and fix problems early, keeping your payment data safe.

Source: Wiz

G2 features reviews on many different vulnerability scanning tools, so choose the one that best suits your needs.

Businesses should also ensure that their staff knows the importance of security. They should share training material about identifying vulnerabilities with their employees and clearly communicate methods for reporting any findings.

Include information about everything in an easily accessible knowledge base. Teach and test new employees on data protection. Make regular testing, such as phishing email tests, part of your IT strategy.

Identity theft, account takeovers, and payment fraud are just a few of the crimes that online shoppers can face. Fraud detection protects e-commerce platforms and their users from financial loss and data breaches. Without automated fraud detection, the volume of manually disputed transactions can quickly overwhelm operations and erode revenue.

Modern fraud detection systems use advanced technologies, like machine learning (ML) and anomaly detection, to analyze large amounts of transaction data.

ML algorithms learn from historical data to recognize patterns associated with fraud. For example, they can detect the repeated use of stolen payment credentials or identify unusual spending habits that may differ from a customer’s norm.

With anomaly detection, businesses can flag transactions that fall outside expected parameters, such as abnormally large purchases or unusual geographic locations, and anomaly detection tools.

Companies can also use real-time monitoring systems to enhance fraud prevention. This involves analyzing transactions as they occur. If they detect potential fraud, they may block transactions or alert stakeholders.

Two-factor authentication (2FA) and multi-factor authentication (MFA) are ways to make accounts and systems more secure by requiring more than just a password to log in.

With 2FA, users need to provide two types of authentication factors. For example, they might enter their password and then type in a one-time password (OTP) sent to their phone. MFA requires three or more factors. In addition to their password and OTP, customers might use biometric authentication, like a fingerprint scan.

Using just a password to protect sensitive information isn’t safe enough anymore. Hackers can easily steal passwords through phishing or other tricks. 2FA and MFA make it much harder for someone to hack into customers’ accounts because they need other information like OTPs and biometric authentication.

OTPs provide a unique code that only works briefly, adding an extra layer of protection. Scanning a fingerprint, face, or even voice ensures only the customers can access the account.

The card verification value (CVV) is a 3- or 4-digit code on a credit or debit card, often found on the back. It’s an important security feature for online and phone payments. The CVV helps confirm that the purchaser has a physical card, reducing the risk of fraud.

Even if hackers steal a customer’s card number in a data breach, they usually can’t get the CVV. That makes it more difficult for them to use the customer’s card.

When a customer makes an online or phone payment, the CVV works with an AVS check. AVS compares the billing address a customer provides with the one their bank has on file.

Real-time verification processes immediately confirm the CVV and address information during the transaction. This helps businesses spot and block suspicious activity before completing a sale.

If a CVV or AVS check fails, the transaction may be flagged or denied to protect against fraud.

3D Secure 2.0 is an advanced security tool that makes online payments safer. It helps confirm that the person making a transaction is the actual cardholder.

When a customer shops online, 3D Secure 2.0 shares secure information about the transaction, like their location or dividing details, with their card’s bank. The bank uses the data to decide if the payment seems safe or risky.

If the transaction looks normal, it goes through without interruptions. But if something seems suspicious, the bank might ask for additional information, like an OTP or fingerprint scan, before approving the payment.

3D Secure 2.0 helps prevent fraud while making the payment process smoother for legitimate customers. It’s a smart way to keep online shopping safe without adding unnecessary steps for most people.

Payment security is an integral part of protecting customer data. Businesses must show their customers that they take their security seriously, and protecting their personal information is an excellent way to demonstrate this.

In a digital world, payment security is vital for running a business. Hackers always develop new methods to break online defenses, so the fight will never end.

But at the same time, your business can use new techniques to ensure payment processing security. Doing so will improve your online reputation and boost customer trust and retention.

Start with the strategies mentioned in this article and follow PCI compliance. That is a great way to secure your payment systems and reduce the risk of costly data breaches.

Beyond security, it's important to optimize payments for seamless transactions. Learn how integrated payment systems drive efficiency and enhance customer experience.

Edited by Jigmee Bhutia

Packed with sensitive data and accessible from anywhere, mobile apps are every hacker's dream.

by Harshit Agarwal

by Harshit Agarwal

Web applications power our online experience day in and day out. We connect, interact, shop,...

by Soundarya Jayaraman

by Soundarya Jayaraman

The Common Vulnerabilities and Exposures (CVE) scan passes. And thankfully, no critical CVEs...

by Abhay Bhargav

by Abhay Bhargav