The quest to understand customer behaviors spans decades.

Different schools of thought dominated in different eras — from Steve Jobs's quip that “A lot of times, people don't know what they want until you show it to them” to Jeff Bezos’s “obsessive focus on the customer as opposed to obsession over the competitor."

Although polar in sentiment, these two statements speak of the same problem: the attitude-behavior gap.

As consumers, we often say one thing and do the opposite. A customer survey might reveal that half of respondents would like a sustainable version of a product. But when you launch one, sales are lower than expected.

In other words, consumers “vote” with their money, and knowing exactly what drives or deters them from making a purchase is key to running a successful business. By linking financial data with other customer insights, businesses can achieve better customer satisfaction and higher operational profitability — and that’s why integrated payments have become a hot subject.

Integrated payments are embedded directly into your company's systems to conduct business, like e-commerce platforms, self-service checkout systems, or point of sale (POS) software.

Integrating payments routes all transactional data to the appropriate location, streamlining the payment process. Your account reconciliation (AR) team doesn’t have to obtain copies of transactions and then go through the tedious reconciliation process. Data from different payment channels auto-sync and are securely stored in one ledger.

Apart from payment processors, POS software can also integrate with CRM software, inventory management systems, customer data platforms, and various business analytics tools.

For example, you can automatically assign recent transactions to a particular customer profile in your CRM, no matter the channel or payment method used.

By integrating payments, businesses reduce manual efforts, improve data accessibility for reporting and analytics, plus elevate customer experience.

Here are five very good reasons to consider payment integration:

For modern consumers, it’s no longer cash or card. It’s also a digital wallet, QR code, a P2P payment app, or a buy now, pay later (BNPL) service.

According to a Paysafe survey, 52% of consumers now feel comfortable leaving the house without a wallet and using Apple Pay or Google Pay for their everyday purchases. For online transactions, more users pay with a credit card stored in a mobile wallet (40%) than a physical card.

Retailers must accommodate these preferences, or they risk losing sales. For businesses operating an ecommerce store, ensuring various payment options can significantly enhance the checkout experience and reduce abandonment rates. Over 40% of US shoppers will abandon a purchase if their preferred method isn’t available. On the other hand, retailers that offer at least three of the most popular payment methods in the given market can increase conversion rates up to 30%.

Integrated payment systems allow merchants to offer a roster of different payment options to consumers without increasing the costs and complexities of account reconciliation. Consumers, in turn, benefit from a sleek, simple check-out experience where they can pay with one click.

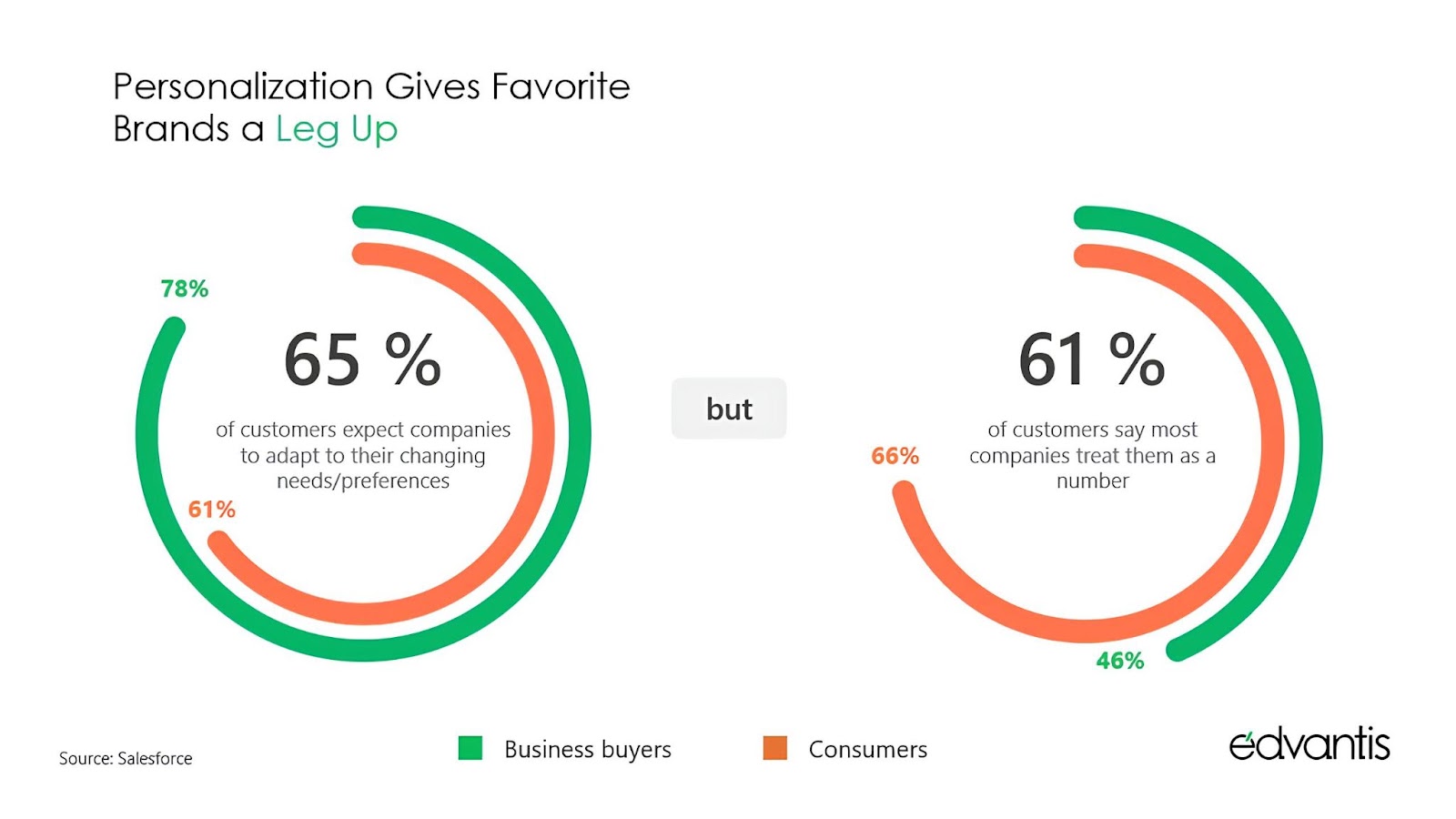

For 80% of global consumers, the experience a business provides is as important as the products and services it offers. However, customers’ ideas of a great experience frequently change, both due to macroeconomic conditions (e.g., inflation, rising cost of living) and personal factors (e.g., a new healthy lifestyle, recent addition to the family).

Companies face the challenge of staying attuned to these shifts and continuing to delight customers with superior service levels.

Source: Salesforce

To better understand customers, businesses adopt a 360-degree view approach — aggregate data from various touch points into a centralized repository to create richer customer profiles and map customer journeys across multiple channels.

For example, by integrating payment systems with CRM software, your teams can automatically monitor:

The use of big data analytics can enable retailers to create customized marketing campaigns based on combined POS and CRM data. This allows retailers to run predictive customer lifetime value (CLV) modeling scenarios, obtain more accurate revenue forecasting, and identify new drivers for optimizing conversions.

For example, e-commerce retailer Zalando developed an attention-based demand forecasting model powered by deep learning. The algorithm can cross-correlated patterns across products and seasons in a data-driven way by assessing on-site customer behaviors, as well as historical sales trends for similar items.

The model then provides highly accurate demand prediction for a horizon of 26 weeks and recommends which level of discounts to apply to each article to increase sales.

Modern shopping is omnichannel.

Customers begin researching a product on mobile, then switch to a tablet to place a pickup order or complete a purchase in-store. Yet, businesses cannot always maintain a clear view of their journeys and provide a unified experience.

That’s because customer data is siloed across multiple non-integrated systems — POS software, inventory management, and retail assortment management applications (RAMA), among others. Because of data silos, an in-store sales associate can’t tell if the customer’s preferred item is in stock, while a customer support agent struggles to process a return request for an in-store purchased item.

A unified commerce approach means integrating data from multiple sales channels (in-store, web, mobile, and social) into a single platform to create homogenous customer experiences across every touchpoint.

Technically speaking, unified commerce requires custom integrations to streamline data exchanges between different business systems, which, in turn, help:

UK fashion retailer River Island implemented a predictive merchandising system to improve its inventory management process. The system automatically aggregates historical sales and stock information and cross-correlates it against current purchase trends.

This predictive system allows River Island to allocate inventory across 250+ store locations. After adopting the new system, River Island saw a 23.7% reduction in stockout frequency for popular products and a 28.3% reduction in lost sales opportunities.

Almost half of consumers say they will likely become repeat shoppers after a personalized shopping experience. However, retailers often miss the mark as they lack full visibility into customers' actions.

This leads to mildly annoying scenarios where shoppers who pick up a product in-store get targeted with abandoned cart emails or bombarded with promo codes for items they never buy.

Transactional data provides a deeper view into when, how, and why customers spend their money, forming the foundation for merchandising strategies and hyper-personalized experiences.

By analyzing transactional and behavioral data, DTC Fashion brand Me+Em discovered that its most valuable customer cohort is omnichannel buyers — people who shop in-store and online. To improve the CX for this segment, the brand launched a “to your door” delivery service. This has helped them increase the average order values, decrease the returns, and improve customer satisfaction.

Integrated payment systems can also help retailers implement dynamic pricing driven by real-time demand and inventory level-set. Leaders can make real-time decisions on discounts and promotion strategies by knowing what’s flying off the physical and virtual shelves at any given time.

Companies that deploy personalization with a large segment of their customer bases also see a reduction in marketing and sales costs by 10% to 20%.

A recent Purchase to Pay Network survey found that 48% of businesses process half or more of their transactions manually. Manual processing adds extra overhead costs, ranging from £2 to £15 ($2.50 to $18.80) per invoice. So if a business processes over 1,000 invoices per month, that’s an extra £1500 in extra costs, easily avoidable with automation.

With real-time payment data synchronization across accounting, ERP, and HR platforms, financial teams can save time and money on manual data entry while simplifying the overall reconciliation process. For example, if your business uses Dynamics 365 platform, you can easily automate invoice management and processing with Power Automate — a low-code workflow automation platform — to improve the speed, efficiency, and accuracy of payment processing.

Beauty retailer Lush used to handle over 120,000 supplier invoices every month manually. Naturally, invoice processing was slow and error-prone. Since adopting an automated system, 92% of the company’s invoices became touchless, i.e., correctly processed without any human input. The new system also allows auditors limited view access for fiscal control, which streamlines compliance.

Financial exchanges are central to every industry, not just retail.

By investing in better payment integration, leaders in the manufacturing, automotive, and healthcare sectors, among many others, can substantially improve revenue cycles, reduce AR costs, and unlock new revenue streams.

Manufacturing companies often have multiple disconnected business systems powering their operations. For example, invoice management and payment processing tools are rarely integrated with ERP software.

Because of that, some companies are unable to accept digital customer payments, leading to delays. On average, manufacturing companies have their invoices paid within 35 days, with almost 20% being paid late, hindering cash flow.

By integrating payment processing into ERP, manufacturers can speed up the pay cycles and attract more sales. Seven in ten B2B customers view online purchases as more convenient and prefer to do so when ready to buy.

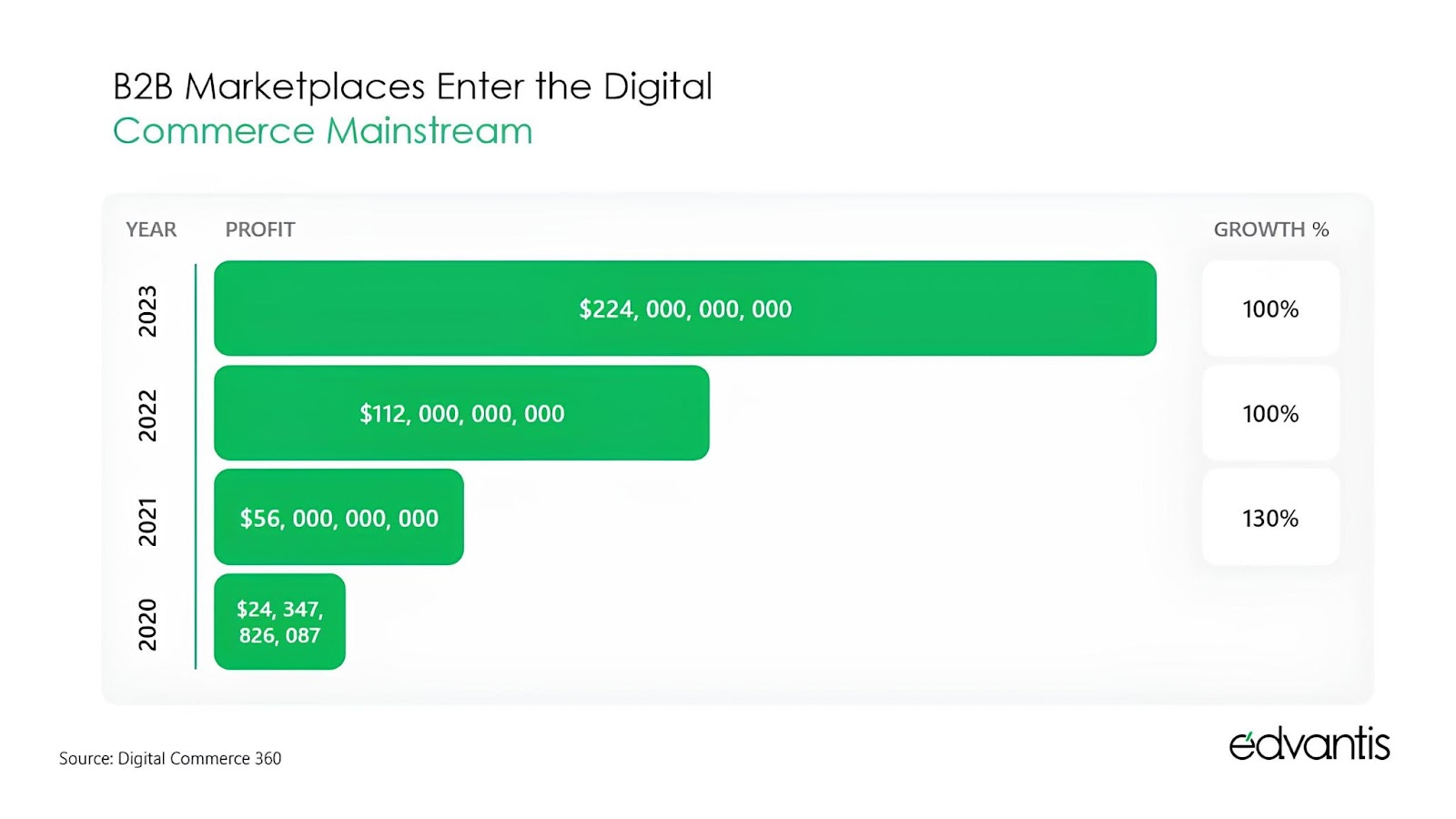

Integrated payment processing is also the first step to creating new revenue flows. For example, launching a B2B ecommerce or servitization offering. Business buyers want to shop omnichannel and increasingly prefer digitally-driven purchase experiences. B2B marketplaces are growing faster than other sales channels.

Source: Digital Commerce 360

In addition, manufacturers are also adopting servitization models. Borrowing the idea from software companies, manufacturers are creating digital, subscription-based offerings to drive recurring revenue.

For example, the Basel Agency for Sustainable Energy (BASE) has been pioneering Cooling-as-a-Service (CaaS) service among heating and cooling OEMs. New industrial clean cooling systems substantially reduce energy consumption and improve air quality and operational productivity. Yet, high upfront costs often deter buyers.

The CaaS initiative encourages OEMs to use a servitization model where the end-user pays for cooling on a per-unit basis. Thanks to CaaS, South African Sovereign Foods could afford to install a new ammonia refrigeration system at its facility, benefiting both from the innovation and cost-efficiency.

Modern connected vehicles are the equivalent of a computer on wheels. So, it’s becoming more common for cars to come equipped with payment capabilities built into their software or infotainment systems.

Embedded payments enable in-car commerce — the ability to pay for various goods and services straight from the infotainment screen without reaching for a card or cash. Already a $75 billion market, in-car commerce covers payments for parking, toll roads, drive-through orders, servicing, and premium infotainment features.

Leading automotive OEMs see premium subscription services as a new revenue channel to supplement car sales. GM expects to make over $25 billion in revenue from in-car subscription services by 2030. Renault expects 20% of its revenue to come from subscriptions and mobility services by the same date.

Integrating payments into connected cars allows OEMs to capture ancillary transactional payment revenues and enable direct sales of new software features to increase their profits.

Few things are as frustrating as dealing with a surprise medical charge or incomplete insurance reimbursement. Such issues often arise when the healthcare provider lacks an effective digital payment collection process.

Consumers have grown to expect a streamlined digital payment experience, allowing them to settle the charges via appointment scheduling software during pre-consultation to point-of-care collections and post-service.

Thus, the initiative to modernize payments for healthcare providers is easier for customer acquisition and retention. A recent InstaMed report found that 66% of patients would switch to a healthcare provider offering a better payment experience.

With an integrated payment solution, the provider can collect fees, such as copayments, as soon as the patient schedules an appointment or immediately after receiving a service. For practices, this improves revenue cycles as you no longer have to wait months until the patient settles an invoice.

Digital payments also allow practices to incentivize faster payment collection. A Bank of America research found that 46% of consumers are likely to take advantage of a lump-sum bill discount, while another 59% are very likely to choose recurring bill payments if these are available.

With integrated payments in healthcare, patients get greater convenience and flexibility, while providers save on payment processing costs and complexities.

The benefits of integrated payment systems are evident. However, businesses still promulgate the implementation. In many cases, the reluctance is driven by three factors: Legacy software, security concerns, and perceived complexities of payment orchestration.

Many businesses rely on traditional back-end payment processors built as a monolithic platform. By design, such systems are hard to customize and integrate with other solutions. They also offer limited capabilities to support new payment features like digital wallet payments or single-use virtual card issuing.

In such cases, businesses eventually choose to migrate to modern payment processing software.

Plug-and-play solutions like Stripe, Square, and GoCardless, among many others, offer access to a host of innovative features and payment methods within one subscription. However, you need to consider the costs associated with accepting different payment methods and compatibility with other business systems.

It’s best to choose a payment service provider offering pre-made integrations via application programming interfaces (API) or software development kits (SDKs). By providing reference architectures and predefined endpoints, APIs enable developers to focus on the business logic of the applications instead of fiddling with the technical details.

Pre-made APIs also come with built-in security controls, ensuring air-tight data exchanges between the linked systems.

All integrated payment gateways must have robust security measures, offering protection against data breaches and malicious hacker attacks. Popular solutions already include the essential security features dictated by the PCI DSS standard.

However, leaders may need to customize the settings further to ensure compliance with other regulations, such as GDPR in Europe or HIPAA in the US, for healthcare companies.

Likewise, all new payment systems must include anti-fraud protection controls. Card not present fraud is a growing problem, expected to cost merchants $49 billion globally by 2030. To stay protected, businesses should adopt strong customer authentication (SCA) policies, 3-domain security, and other forms of multi-factor authentication.

Automatic solutions for transaction monitoring and fraud detection are also necessary. For these tasks, merchants increasingly choose machine learning-based solutions to replace older, rule-based systems. ML fraud detection engines can parse large data volumes in real time and more accurately detect suspicious transactions. State-of-the-art systems deliver 96% to 99% accuracy rates for ecommerce transactions.

Global merchants often rely on multiple payment partners in different markets. A large and complex portfolio of payment processors can be hard to manage effectively without a payment orchestration layer.

Payment orchestration is a mechanism for integrating different payment service providers, banks, and acquirers in a unified software processing layer to automatically oversee, manage, and execute end-to-end payment processing.

Effectively, payment orchestration centralizes all payment processing, reporting, and reconciliation into a single interface. This allows teams to run analytics against aggregated data to better track key metrics and obtain more comprehensive data for decision-making.

For developers, a third-party orchestration platform reduces the complexities of integrating and maintaining multiple payment integrations. For operational teams, orchestration platforms centralize governance and automate the application of unified business logic for routing, approving, and settling various transactions.

Integrating payment systems with CRM platforms, MarTech tools, and business analytics products offers a deeper understanding of customer behavior and preferences.

With access to purchase history and customer profiles, businesses can personalize marketing efforts, offer targeted promotions, and enhance overall customer engagement. This not only fosters loyalty but also drives repeat purchases and boosts revenue.

As technology continues to evolve, embracing payment integrations will be essential for businesses looking to thrive in the digital era.

Don't miss out on the wave. Learn how digital payments are shaping the global payment industry.

Edited by Sinchana Mistry

The global economy is undergoing significant shifts with high interest rates, increased...

by Evie Parker

by Evie Parker

I believe getting paid should be a simple, straightforward process, not a stressful one.

.png) by Tanuja Bahirat

by Tanuja Bahirat

Our digital world has made it easier to do business across borders and around the globe.

by Marwan Forzley

by Marwan Forzley